IBM

- joe14085

- Feb 4

- 6 min read

IBM's Remarkable Comeback: How Big Blue Reinvented Itself in the AI Era

One of the oldest names in technology, IBM, is staging a surprising comeback that's catching the attention of investors and tech enthusiasts alike. Once considered a sluggish giant overshadowed by flashier tech firms, IBM has seen its shares soar near record levels. The question arises: what really stands behind this resurgence? A bold shift in focus from hardware to software and artificial intelligence (AI) was at the core of the turnaround. However, it's important to note that these improvements have only become visible over the past five years, and IBM is still far from where it was 20 years ago on a relative basis.

Outpacing the Tech Titans

IBM's share performance has been remarkable. Its stock climbed 26% this year, outperforming well-known tech giants like Apple, Microsoft, Amazon, and Alphabet. As of a recent trading day, IBM's shares hit their highest level since 2013. This upward trend indicates renewed investor confidence, and it's even more striking considering IBM's comparatively lower valuation.

For the past 2 years IBM share price has managed to outperform the SP500 Index and 2 of its direct competitors in hardware and consulting businesses.

Currently, IBM is valued at less than 20 times its forward earnings, which is lower than the Nasdaq 100's multiple of about 24. Additionally, IBM offers a dividend yield of around 3.3%, one of the highest in the S&P 500 information technology index. This has contributed to drawing investors looking for value and returns.

But IBM's resurgence isn't just about rising stock prices—it's also about financial efficiency, demonstrated in its improved Return on Invested Capital (ROIC). In 2024, IBM recorded an ROIC of 8.5%, exceeding both its own historical average of 7% and the industry average of 3.2%. This suggests that the company has become much more effective at generating profit from the capital it invests. However, this ROIC improvement still lags behind the levels IBM achieved in its prime years.

Riding the AI Wave

IBM revenue worldwide from 2010 to 2023, by segment

Even though IBM has seen way better revenue levels, there are reasons to be optimistic about the old company. Source of the image: Statista

IBM's transformation wasn't merely financial; it was strategic. The company shifted its core focus to software and AI, both areas witnessing rapid growth. In its latest earnings report, IBM revealed that software revenue grew by 10%, with its Red Hat division—acquired in 2019—posting growth of 14%. Moreover, IBM's book of business related to generative AI surpassed $3 billion, rising by more than $1 billion within just one quarter. These investments and revenue figures signal IBM's successful pivot to emerging technologies.

ROIC Difference: Why It Matters

ROIC measures how efficiently a company uses its capital to generate profits. For IBM, this metric is a crucial indicator of its turnaround. IBM's strategic shift from hardware to software and services significantly boosted its ROIC. Unlike hardware, which tends to have low profit margins, software and consulting deliver much higher returns, especially when supported by long-term contracts. By moving away from low-margin businesses and focusing on recurring revenue streams, IBM has ensured a more stable cash flow. This stability has allowed the company to innovate without overextending its resources.

Comparatively, the average ROIC in the industry is 3.2%, but IBM has managed to bring it up to 8.5%. This success can largely be attributed to its strategic focus on capital efficiency—concentrating on software that yields high margins while maintaining operational effectiveness. Nevertheless, it's important to recognize that IBM's ROIC is still below the levels seen in its historical peak years.

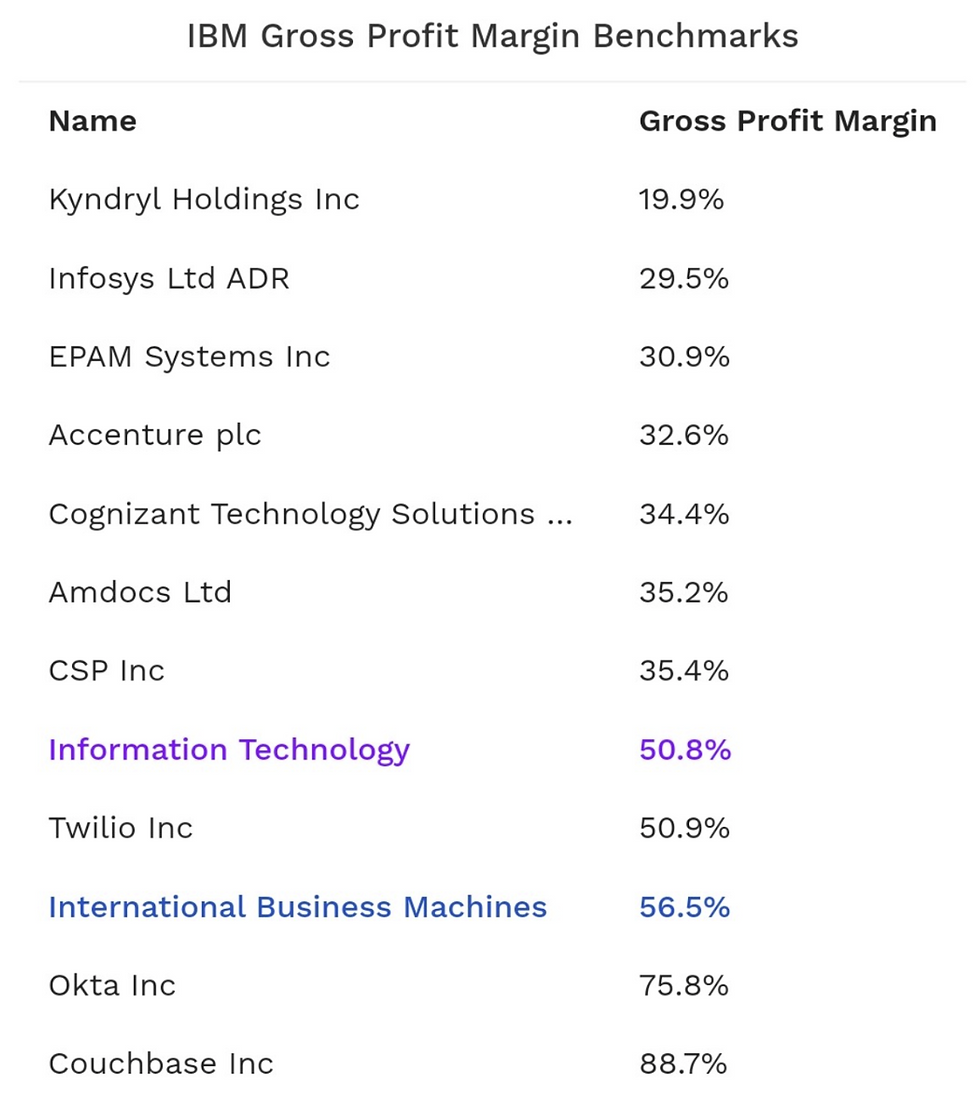

Capital Efficiency, EBIT, and Rising Margins

IBM's focus on capital efficiency is evident in its margins. In the latest quarter, IBM expanded its gross margin by 210 basis points and its operating pretax margin by 100 basis points. The company's software segment, for instance, achieved a profit margin of about 30%. The decision to divest lower-margin, hardware-centric divisions allowed IBM to direct resources where they would have the most impact—in high-margin cloud services and AI solutions.

Examining EBIT (Earnings Before Interest and Taxes) and operating margin data over time, it's clear that IBM's financial health has improved, but it still has a long way to go compared to its historical performance. In 2009, IBM's EBIT was significantly higher than it is today, reflecting the company's greater profitability back then. While recent years have seen some recovery, the current levels remain far below the peak EBIT and operating margin figures from the past. This highlights that while IBM is on the path to recovery, it is still rebuilding its profitability to match former levels.

Source: Finbox

IBM margins can be easily considered healthy regarding the size of the company, its diversification and the increased competition it is facing on every sector.

The strategic spin-off of non-core units like Kyndryl, which took over IBM's managed infrastructure services in 2021, enabled IBM to focus more intensively on cloud and AI offerings. Red Hat’s open-source approach further helped IBM become more agile, driving cost efficiency and productivity.

Internal Challenges, Not the Market

IBM's challenges were internal rather than a reflection of market conditions. The broader technology market has remained robust, but IBM had become too reliant on legacy hardware while the rest of the industry shifted to cloud-based and software services. The company also faced economic uncertainties and a slowdown in client spending on consulting services. The key insight was recognizing that the issue wasn't the market itself, but rather IBM's internal strategy and direction.

Addressing these issues required divesting from legacy hardware businesses and investing heavily in high-growth segments—namely software, AI, and cloud services. IBM understood it needed a complete pivot and made bold moves to achieve this.

Strategic Moves to Solve the Problem

IBM's turnaround wasn't an accident. It came from deliberate actions taken by its leadership. One of the boldest moves was the $34 billion acquisition of Red Hat in 2019. This gave IBM access to Red Hat's hybrid cloud expertise, effectively making it a key player in enterprise cloud solutions. Additionally, IBM expanded partnerships with cloud providers like Amazon Web Services (AWS), which increased the reach of IBM's software products.

The impact of these moves was profound:

Acquisitions: The acquisition of Red Hat doubled its revenue to $6.5 billion and boosted IBM's hybrid cloud capabilities. IBM has also announced plans to acquire HashiCorp to further bolster its software portfolio.

Innovation: Investments in AI models, such as the Granite family, resulted in more efficient enterprise AI solutions. These models were 90% more cost-efficient to train and could be tailored in weeks, not months.

Financial Results: IBM's software revenue growth accelerated to 10%, while its Hybrid Platform and Solutions Annual Recurring Revenue (ARR) grew by 11% year-over-year to $14.9 billion.

A Blueprint for Reinvention

IBM's comeback demonstrates how a legacy company can reinvent itself in a fast-evolving industry. By recognizing its internal shortcomings, making decisive investments, and focusing on high-margin segments, IBM managed to increase its ROIC, boost sales, and significantly enhance its share performance compared to the market. From a 26% rise in stock value to higher-than-industry returns, the impact is clear.

The company has still a lot to do when it comes to improving its ROIC, however, it's also evident that IBM is still in the process of catching up to where it once was. The improvements over the past five years are significant, but the company remains distant from the peak performance it enjoyed two decades ago. The path forward requires continued strategic investment and focus.

The company's ability to pivot toward hybrid cloud and AI, combined with a willingness to divest from non-core areas, serves as an important lesson for other legacy firms. When faced with stagnation, a focused strategy and a willingness to adapt can turn even a seemingly sluggish giant into a leader of innovation once again.

IBM's journey is a case study in leveraging capital efficiency, smart acquisitions, and strategic partnerships to evolve with the market. As technology continues to change at lightning speed, the ability to focus on core strengths and adapt to new realities will determine which companies thrive and which get left behind.

References

Comments